Our Demands

Burning fossil fuels is the primary cause of climate change. The Oregon Treasury continues to invest in these fossil fuels, therefore Divest Oregon demands of the Oregon Treasurer and the Oregon Investment Council:

Invest in a just, climate-safe future

End investments in fossil fuels

Address climate risk transparently

How We Make Progress

What's New

Photo by SpaceX on Unsplash In a July 1 article Reuters reported that Oregon Treasurer Steiner wanted guidance from the federal Securities and Exchange Commission (SEC) about SpaceX. How should pension funds handle the new company with the giant market valuation? SEC Commissioner Mark Uyeda answered Elizabeth Steiner in an interview in Reuters . One takeaway is his simple point that if you don't like the governance arrangements of a stock, don't buy it. A message from the SEC's Uyeda: If you don't like SpaceX's governance, don't buy the shares ( Reuters Sustainable Finance , July 1, 2026) Note: The Oregon State Treasury has $6.8 million in exposure to SpaceX through one public equity index fund and one global equity portfolio ( Portland Business Journal July 2, 2026). Divest Oregon has made the same point to Treasurer Steiner, repeatedly. For example, Treasurer Steiner posted on Facebook on May 6, 2026 that she is “deeply troubled” by the ways ICE contractor Geo Group fails to adhere to Oregon Investment Council (OIC) policy. Divest Oregon responded : The Oregon Treasury has held stock in private prison/immigrant detention contractors for years, in spite of well-publicized abuse. If a company is violating OIC policy the Treasury has an obligation to sell the stock. In fact, Treasury’s screening process can and should prevent purchasing or holding stock that violates OIC/Treasury standards. The SEC Commissioner quoted in the Reuters ’ interview about SpaceX also says pension funds have the duty and ability to do such screening: Question by Reuters to SEC Commissioner Uyeda: "You write that ‘If prospective investors have concerns with the governance arrangements, then their most powerful tool is to not purchase shares of the stock.’ But critics like some big pension funds say the fast-track addition of SpaceX to big indexes could make them unwilling buyers of the stock. What would you say to such critics? Response from SEC Commissioner Uyeda: "Large pension funds have choices with respect to their investment decisions as part of their fiduciary duty to the plan. While index funds may have certain conveniences and low costs, there is a trade-off to outsourcing securities selection to a third party. There are alternatives, such as selecting a fund that follows a different index or is actively managed, or engaging in customized direct indexing that would provide more control over the portfolio.”

A Geo Group van leaving the Northwest ICE Processing Center in Portland Oregon. May 2026

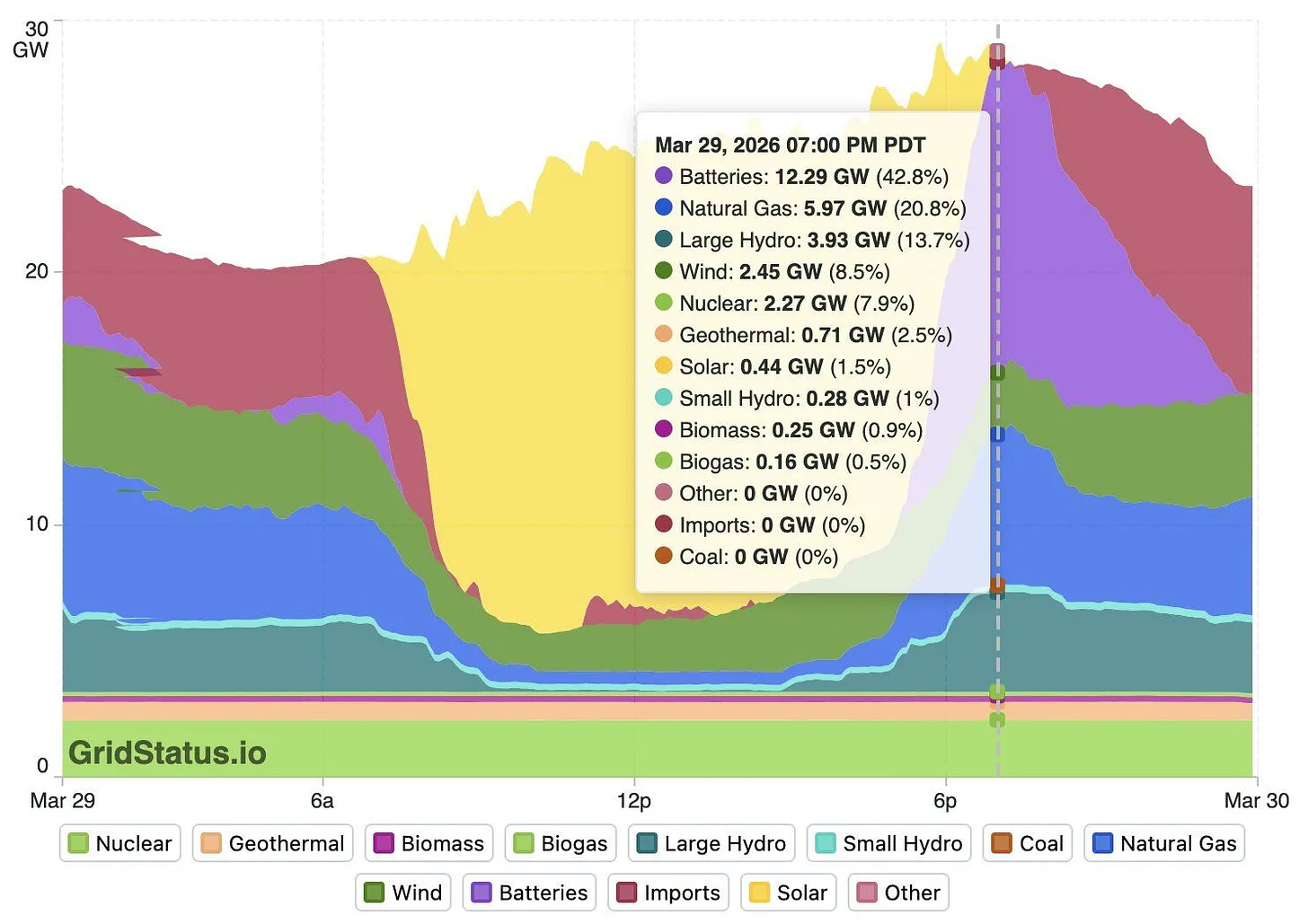

At the March 2026 OIC meeting, John Goldstein from Goldman Sachs spoke of the strength of renewable energy stocks (recap in Net Zero Investor 5/3/2026 ). Bill McKibben shows us how the sector is evolving with battery technology advances. Night into Day ( The Crucial Years substack 3/30/2026): “For the first time, the United States now has the capacity to supply 100% of domestic energy storage project demand with American-built systems,” said Noah Roberts, executive director of the U.S. Energy Storage Coalition. “That is a fundamental shift from where we were just a year and a half ago, when the majority of battery storage systems were imported.” “Already, the U.S. has enough capacity to meet demand for finished grid battery enclosures…. By the end of this year, the U.S. will also achieve self-sufficiency in a higher-value part of the supply chain: the battery cells themselves. It’s a major industrial coup that is bringing thousands of high-tech manufacturing jobs to communities across the country.” Solid-state batteries are becoming a possibility; they promise to solve several problems: “Batteries are now being tested by multiple companies that can go 800 miles on a single charge….“In September, Mercedes drove a modified EQS over 1,200 km (745 miles) using 106 Ah solid-state battery cells supplied by US-based Factorial Energy. Factorial launched the first commercial solid-state battery program in the US …earlier this year.” The Finnish company Donut Labs shows where this is heading: “The Donut batt can charge to full in five minutes…; has a practically unlimited lifespan (100,000 charging cycles); is unaffected by heat and cold (-30C to 100C); and contains no rare earth, precious metals or flammable liquid electrolytes. With all that, Donut Lab says it will be cheaper to produce than conventional lithium-ion batteries…” “And the technological miracles are only beginning. For instance, Christopher Mims reported last week in the Journal on a new round of ‘thermal batteries that store solar power as heat instead of electricity, perfect for use in high-temperature industrial processes.’” “Marija Maisch was reporting in January that…salt-based batteries are nearing price and performance parity, if not for cars then for utility scale batteries.” And this chart shows the surge of batteries coming online as solar installations lose sunlight. Night into day.

A question from Divest Oregon, a coalition of a hundred organizations with strong PERS representation, remains unanswered: What screening process does the Oregon State Treasury (OST) use, if any, when investing PERS funds or choosing investment managers? Is the Treasury screening investments in fossil fuel companies? Andrew Bogrand, Divest Oregon’s Communications Director, spoke at the Oregon Investment Council (OIC) in January 2026. He noted that investment in fossil fuels contributes to global instability, using Venezuela as an example. (See this blog .) The current Iran war emphasizes this point. Andrew regularly comments on the ties between insecurity and fossil fuels as a policy lead for human rights and natural resource justice at Oxfam. The argument that fossil fuel investments are a sensible diversification of a portfolio has long been outdated. But looking at the most recently published June 2025 public equity and fixed income data, the Treasury is still investing in fossil fuels. Under fiduciary duty and the Climate Resilience Investment Act ( CRIA ), the Treasury must move to alternative investments that align with the reality of climate change and a rapidly destabilizing world. Is the Treasury screening investments prone to legal liability, human rights abuses, or reputational risk? In an April 2023 report , Divest Oregon called out the Treasury's investment in private prisons and surveillance technology as context for the question: Does the Treasury have a screening process? If so, what is the screening process? One example given in that report was the NSO/spyware technology that OST heavily invested in. The Guardian reported extensively (2022) on the OST’s investment in NSO/Pegasus spyware: “However, it now appears that the Oregon pension fund, one of the most prominent in the US, gave its tacit approval over an investment in NSO several years ago – at a time when security researchers were already publicly raising alarms about the company.” In a more recent report, Oregon Treasury’s Investment Screening Failures ( October 2025 ), Divest Oregon again questioned the Treasury’s investment screening process. Examples of questionable investments included GEO Group, CoreCivic, and Palantir. Investments in GEO Group and CoreCivic fund private prison contractors and ICE detention centers. Investment in Palantir funds ICE surveillance software used against US residents. See additional information below for each of these companies. The most recent public data ( June 2025 ) shows that the Treasury continues to invest in these private prison and surveillance technology companies with a long history of human rights abuses and legal vulnerability. These companies are central to the current federal administration’s construction of a police state and its massive violation of due process. See Trump’s Mass Deportation Campaign ( The New Yorker 3/15/2026). For example: Recent private prison contractor GEO Group news: In February 2026, the Supreme Court found that GEO Group, a private prison operator running an Immigration and Customs Enforcement (ICE) facility, cannot claim governmental immunity from lawsuits for violating human trafficking laws, even if those violations were under government orders. Recent surveillance technology company Palantir news: In Portland, now, Palantir’s Elite app is being used to identify potential deportation targets, generate dossiers on individuals and provide a “confidence score” on the person’s address. ( The Guardian 3/13/2026) Why should the Treasury screen its investments? Screening is necessary to avoid investments that contravene Treasury standards, OIC policy, legal standards including fiduciary duty, or Oregon State law. For instance: The Oregon Department of Justice has recently opened an inquiry as to whether OST investment in companies with contractual ties to ICE violates the Oregon Sanctuary Promise Act of 2021 . The CRIA Act of 2025 mandates that the Treasury: -- “actively analyze and manage” climate risk to the portfolio -- report on its progress toward investing in public equity holdings that incorporate the tenets of a just transition in their overall priorities and portfolio